Conflict in the Middle East: The perfect storm for price gouging in Africa

24 March 2026 by Carin Smaller, Executive Director of the Shamba Centre

The attack on Iran by the U.S. and Israel, the Iranian response, and the subsequent closure of the Strait of Hormuz, have shaken global energy and fertilizer markets. Crude oil is now nearing USD 120 a barrel and fertilizer prices are spiking, with urea prices surging by 60%. Much has already been written about the global dependency on fuel, fertilizer and gas from the Persian Gulf States and the potential impacts on food security (see FAO and IFPRI). Ultimately, the impact on production costs and crop yields will depend on how long the Strait of Hormuz remains at a standstill.

As with previous shocks, most recently the COVID-19 pandemic and the Russian invasion of Ukraine, supply chains will be re-routed as companies and countries seek alternative sources to compensate for shortfalls. But given that the Persian Gulf States account for an estimated 30% of the global fertilizer trade, the financial strain placed on farmers and, ultimately, consumers will be high. The risk of another food security crisis looms large.

The consequences of dysfunctional markets

In well-functioning markets, the crisis could be short-term. Alternative suppliers will fill the gaps, and prices will return to normal levels. Unfortunately, this is not the case where markets are dysfunctional. In highly concentrated markets, companies can exercise their market power to set prices, leading to price gouging and profiteering. All too often, companies will use the excuse of a global crisis to raise prices. While these price increases may be justified to account for a rise in supply chain costs, this is no longer the case when costs decrease.

A sellers’ inflation is possible in highly concentrated and uncompetitive markets where large firms set the prices. The persistent food price inflation experience by most low and middle-income countries after the COVID-19 pandemic, and in some cases continue to experience, illustrates market dysfunction given that input costs and commodity prices have fallen back to pre-COVID levels.

When a crisis strikes, the immediate risk of price gouging mounts. This is already happening at the petrol pump in most countries where companies have transferred price increases onto consumers within days of the conflict breaking out despite selling petrol that did not just arrive from the Persian Gulf. In well-functioning markets, like in Australia and Ireland, within days, competition authorities put these companies on notice, announcing plans to monitor price gouging and intervene as necessary.

A close eye on fertilizer prices

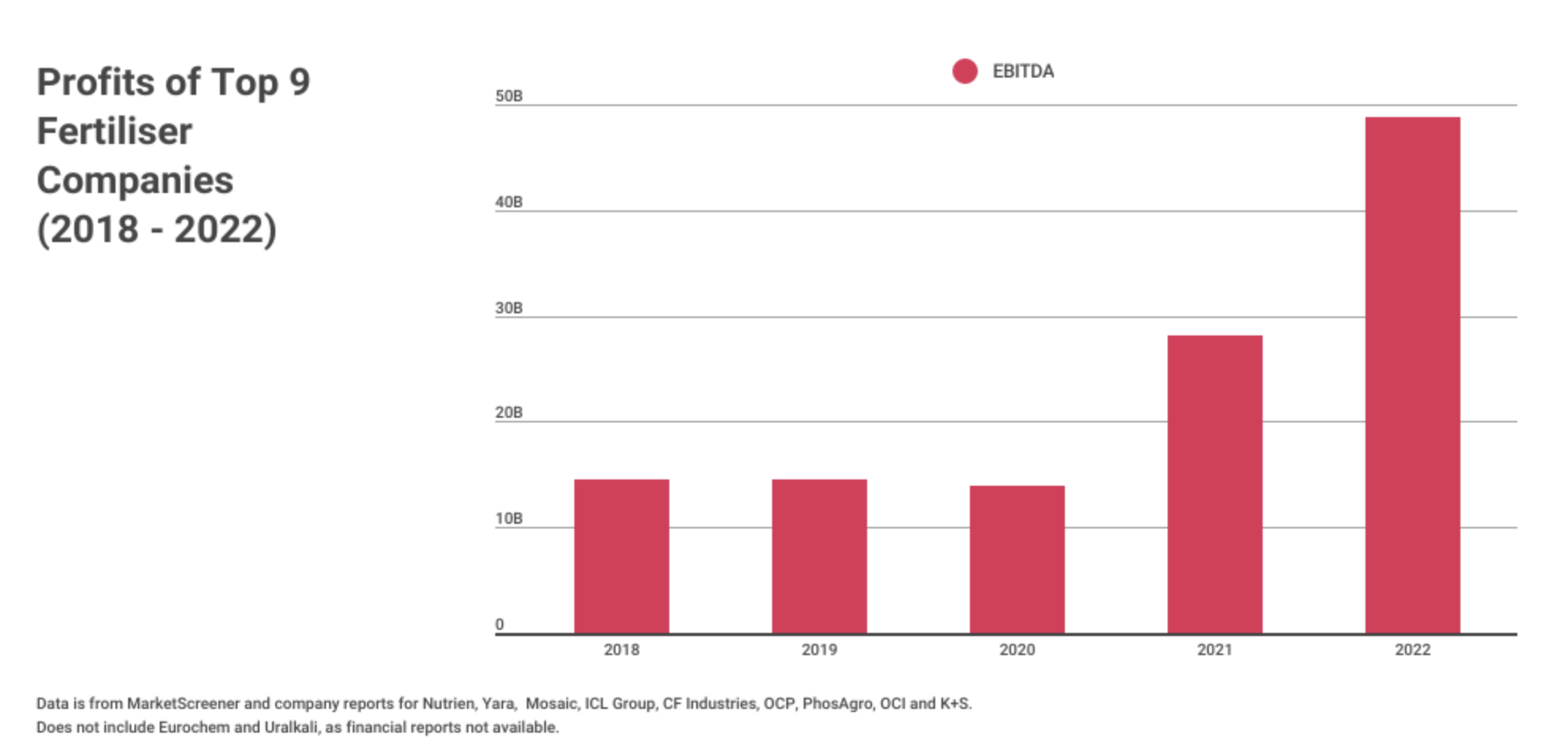

Energy and fertilizer markets are highly concentrated and at serious risk of price gouging by dominant firms. In 2022, the fertilizer prices spiked in response to the supply constraints from the Russian invasion of Ukraine. However, according to a study by the IATP, fertilizer companies increased prices far beyond the increase in production costs. Rather, the top 9 fertilizer companies boosted their profit margins to 36% in 2022 (see Figure 1).

“Fertilizer companies increased their profit margins significantly in 2022”

Figure 1. Profits of top 9 fertilizer companies, 2028-2022. Source: IATP

Fertilizer prices have since decreased from their high prices in 2022, however, they nonetheless increased by 18% in 2025. While the World Bank claims that the increase is the result of trade restrictions, strong demand and production shortfalls, market power likely plays a role.

Implications for African fertilizer markets

In sub-Saharan Africa, few countries produce fertilizer. Prices are largely determined by the costs of imported fertilizer combined with the margins associated with transport, port charges, blending and processing. Reliance on fertilizer originating from Persian Gulf region varies by country with UNCTAD highlighting a dependency of 31% in Tanzania, 26% in Kenya, and 22% in Mozambique.

Because fertilizer markets in eastern and southern Africa are oligopolistic, the opportunity for price gouging is already enormous. According to research by the African Market Observatory, only two to five large suppliers are able to source fertilizer internationally in bulk. These suppliers are vertically integrated, from international production through to distribution across the region. This concentration is further reinforced by the high barriers to enter the market.

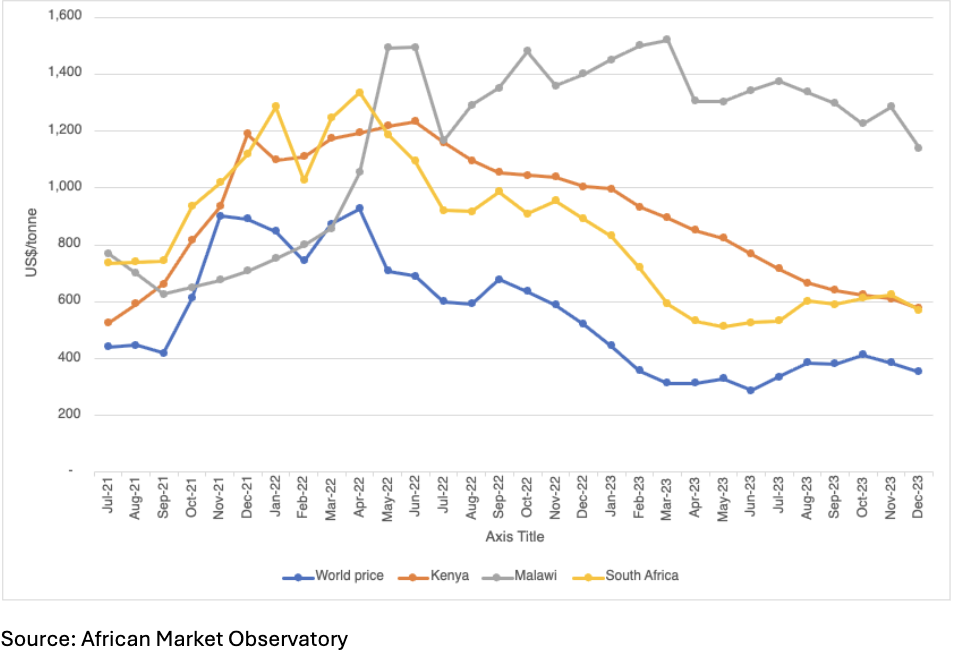

This uncompetitive, oligopolistic fertilizer market helps explain why fertilizer prices in Africa have remained high since the worldwide spike in 2022. While fertilizer prices across the region increased along with international prices in late 2021, they did not decline alongside international market prices (see Figure 2).

“The high price of fertilizer in sub-Saharan Africa suggests anti-competitive behaviour by vertically integrated companies ”

Figure 2. Price of urea in Kenya, Malawi and South Africa compared to world prices between 2021 and 2023

The high prices harm farmers, governments, and donors which subsidize fertilizer access. High fertilizer prices had a direct impact on the record-high food prices in 2021 to 2023 with those in low- and middle-income countries bearing the harshest burden of soaring food prices given that they spend a larger portion of their incomes on food.

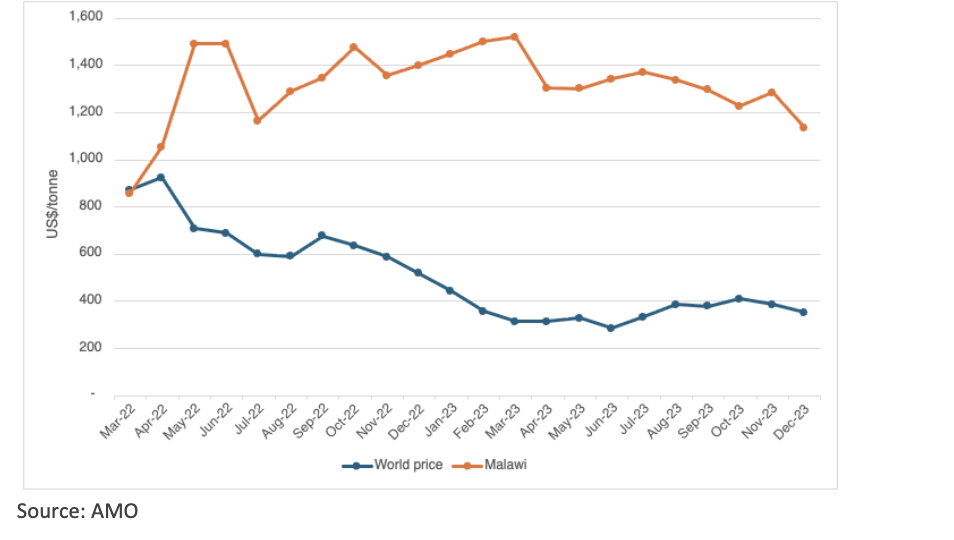

If the conflict continues and the fertilizer prices spike further, this could decrease production yields in the next growing season, and trigger another food security crisis. This happened in Malawi in 2022. At the time, the price of fertilizers in Malawi was up to four times higher compared with world prices (Figure 3). Up to 70% of smallholder farmers in Malawi cited costs as the main factor for their reduced purchase and application of fertilizer in 2022 which directly ties the low maize harvest in Malawi in 2023. While many blamed the devastation caused by Cyclone Freddy for the low yields and subsequent rise in hunger, the cyclone is estimated to have impacted only 10% of crop production. Rather, the high fertilizer prices in Malawi are directly linked to the monopoly power that exists in the fertilizer markets across Africa.

“Fertilizer prices in Malawi were up to four times higher than world prices in 2022 and 2023 ”

Figure 3. Price of urea in Malawi compared to world prices between 2022 and 2023

African regulators can take action

African competition authorities can intervene now to minimize this harm. Nearly half of countries in sub-Saharan Africa have competition laws, policies and institutions in place, with others covered by regional competition authorities. Some institutions have operated for less than 5 years, but others have more than 10 years of experience (see Shamba Centre). While many do not have sufficient technical or financial capacity to respond to the myriad of challenges, they can take action if provided with appropriate support.

Using the African Markets Observatory (AMO) monthly monitor of fertilizer prices, competition authorities can access the data to determine whether price gouging is occurring and to what extent. The Agrifood Anti-Monopoly Tracker can alert competition authorities about anti-competitive behaviour in neighbouring countries that may also impact their markets.

The Iran war may be a perform storm for price gouging, but African competition authorities can minimize the harm and continue to use competition law and policy as a tool for ensuring functioning markets that are able to deliver fair prices.